By Keel Research Team · Updated May 12, 2026

Funding Carry Strategy on Hyperliquid

Short the Hyperliquid perpetuals paying the highest funding, hedge the directional exposure with spot or another long perp, collect the funding rate as yield. The classic crypto carry trade, sized for Hyperliquid's hourly funding cadence.

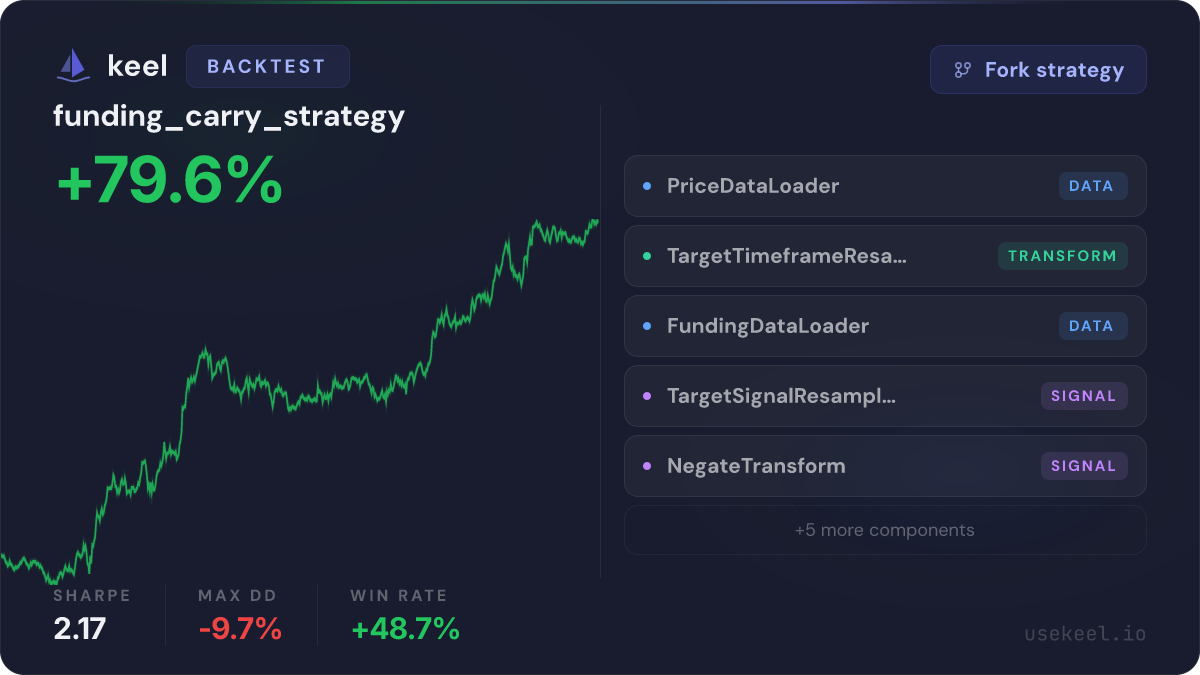

Live backtest reference. Numbers below are from a public Keel backtest you can open and fork directly: funding_carry_strategy on Keel ↗. Backtest run on May 11, 2026 across the period August 15, 2024 – April 30, 2026.

What is funding carry?

Funding carry is a delta-neutral strategy that monetizes the funding rate on perpetual futures. When a perpetual trades above its spot oracle, the protocol charges longs a small hourly fee that gets paid to shorts; when it trades below, shorts pay longs. The strategy is to be on the receiving side of that flow — typically short the perp when funding is positive — while hedging the directional exposure with spot or another long position so net market exposure is near zero.

On Hyperliquid, funding settles every hour. That cadence matters: positive funding regimes can persist for hours to days on the same pair, especially in trending markets where directional traders crowd long. A short-perp + long-spot pairing earns the funding rate, compounded hourly, less the cost of carrying the spot side (which on HL is just the spread + execution fees, since spot is custodial on-chain).

The trade isn’t risk-free — funding flips, perp-vs-oracle basis fluctuates, and sharp price moves can hit margin on either leg. But on liquid HL pairs with persistent positive funding, the carry has historically been one of the cleanest yield sources in crypto. The pipeline below is how Keel automates the trade end-to-end.

How it works — pipeline

The Keel pipeline runs four stages every cycle:

Stage 1

Data

PriceDataLoader + FundingDataLoader pull price + hourly funding across the HL universe. TargetTimeframeResample aligns price to the strategy's target bar.

Stage 2

Signal

TargetSignalResample maps funding rate onto the same timeframe. NegateTransform flips the sign — positive funding becomes a short signal (collect funding by being short the perp).

Stage 3

Sizing

Risk-budgeted weights across qualifying pairs. Per-pair notional capped by drawdown tolerance; total exposure scaled to target portfolio volatility.

Stage 4

Execution

Funding-aware order placement with hourly re-evaluation. Rotate out of pairs whose funding drops below threshold; rotate in pairs that cross above.

The full component graph (including 5 more stages not listed above) lives in the live Keel backtest — click through to inspect each stage, change a threshold, or fork the strategy.

Backtest snapshot

Sharpe

2.17

Total return

+79.6%

Max drawdown

-9.7%

Win rate

48.7%

Period: August 15, 2024 – April 30, 2026. Sourced from this live Keel backtest · run on May 11, 2026.

Click the chart to open the live backtest on Keel.

When it works, when it fails

Works: in regimes where directional flow is persistent — bull markets where long perps are crowded for weeks at a time, or trending alt-cycles where new entrants chase the move. Funding rates stay elevated, the carry compounds hourly, and the hedge keeps you neutral on the underlying. Historical win rates have been highest in periods of sustained positive funding across multiple liquid pairs.

Fails: around regime turns. A pair carrying 100% APR can flip to flat or negative inside hours, often on a news event or liquidation cascade. The strategy gets caught between funding turning against it and a sharp basis move. The Keel pipeline mitigates this with hourly re-checks and a funding-trajectory filter (funding has to be persistently positive over the last N hours, not just spiking now), but it doesn’t eliminate the risk.

Tail risk: a market-wide volatility event can hit both legs of the hedge simultaneously — your short perp gets margin-called on a price spike, your long spot can’t cover the gap. Position sizing relative to portfolio-level liquidation distance is what separates a profitable carry strategy from one that blows up.

Fork this strategy

Open the strategy in your own Keel workspace. The pipeline, signals, sizing rules, and execution logic are all editable. Run your own backtest with custom parameters, optimize, then deploy live to Hyperliquid with one click. Free to start — connect a Hyperliquid wallet when you’re ready to go live.

This strategy documentation is informational and based on historical backtest data. Past performance does not guarantee future results. Perpetual futures with leverage can result in losses exceeding initial margin. Not financial advice.

Automate it

Trade systematically on Keel

Keel is a Strategy OS for AI-assisted systematic trading on Hyperliquid. Backtest, optimize, and run live strategies across single-stock perps, indices, and crypto majors — realistic fees, slippage, and funding modeled.

Free to start — connect a Hyperliquid wallet when you’re ready to go live.

What you can do

- Backtest any strategy with realistic fees, slippage, and funding.

- Optimize parameter grids by Sharpe, drawdown, hit rate.

- Deploy live to HL with stops + position limits + funding-aware execution.

- Iterate with AI — describe a thesis, get a tradeable pipeline.

FAQ

Funding carry — questions

What is funding carry, in one sentence?

Funding carry is the strategy of being short a perpetual when funding is heavily positive (longs paying shorts), hedged with a long position in spot or another perpetual, so you collect the funding rate as yield while staying delta-neutral.

Why does carry exist on Hyperliquid?

Funding rates exist to anchor perp prices to the spot oracle. When directional traders crowd long, the perp trades above oracle and funding goes positive — longs pay shorts. As long as that crowding persists, a short-perp hedged with long-spot trader earns the spread. The strategy is monetizing the cost of being on the crowded side of HL's perp book.

What are the main risks?

Three. (1) Funding flips — a 100% APR rate can collapse to flat or negative inside hours. (2) Basis risk — the perp can diverge from oracle while you're hedged, producing mark-to-market drawdowns even as funding accrues. (3) Liquidation cascade — sharp price moves can hit margin on either leg of the hedge if sizing isn't conservative. Position sizing and per-asset funding-rate persistence checks matter more than picking the highest-APR pair.

How is this different from running it manually?

Manually, you'd watch funding rates, pick a pair, open a short, open a hedge, monitor funding settlement, and roll the position when conditions change. The Keel pipeline does each of those programmatically: signal selection from the screener cohort, position sizing per risk budget, execution with funding-aware order routing, and automated re-balance on regime change. The backtest below is the historical performance of that automated pipeline, not a manual mental walk-through.

Can I customize parameters or run my own variant?

Yes. Fork the strategy into your own Keel workspace, then adjust universe, funding threshold, volatility filter, position sizing, or any other parameter. Run the modified backtest, optimize across parameter grids, and deploy live if it improves. The strategy template is a starting point, not a fixed product.

Related

Funding Rate Screener

Live screener for HL pairs paying the most carry — high funding combined with low volatility. The starting cohort for this strategy.

Funding Leaderboard

Top 30 HL perps by current 1h funding rate, annualized. The data this strategy reads to pick its cohort each cycle.

All strategies

Documented strategy library — more strategies (trend following, cross-sectional momentum, stat-arb) shipping soon.